Your Credit Kaagapay Guide to the Most Cost-Efficient Cards in the Market Today

Choosing the right credit card is one of the smartest financial decisions you can make—especially if your goal is saving money, avoiding unnecessary fees, and stretching your budget responsibly. In the Philippines, where many cardholders pay the maximum allowable interest rate and shoulder yearly renewal fees, picking a card with low interest and No Annual Fee for Life (NAFFL) can lead to thousands of pesos in savings each year.

This Credit Kaagapay guide analyzes the Top 5 Credit Cards in the Philippines offering the best combination of:

- Lowest interest rates (2.00%–3.00% monthly)

- No Annual Fee for Life (NAFFL)

- Friendly fee structures (zero late fees, zero overlimit fees, rebates, etc.)

- Practical benefits for real Filipino consumers

Whether you’re a first-time cardholder, a budget-conscious employee, or someone looking for a long-term credit partner, this list gives you clear, data-backed options worth considering.

Market Context: Why Low Interest + No Annual Fee Matters

Credit card costs in the Philippines are governed by the Bangko Sentral ng Pilipinas (BSP), which sets a ceiling on how much banks can charge customers. As of the latest review, the BSP cap is:

🔹 3.00% per month finance charge

Any card offering a rate below this benchmark—such as 2.00% or 2.50%—is considered a low-rate credit card, offering real savings to customers who occasionally carry a balance.

At the same time, credit cards typically charge ₱1,200 to ₱4,000 in annual renewal fees. A card with NAFFL removes this recurring cost entirely, making it free to own forever, regardless of usage.

In short:

- Low interest → protects you when you can’t pay in full

- NAFFL → protects your wallet every year

- Both combined → maximum long-term savings

Summary of the Top 5 Credit Cards (2025)

Ranked based on interest rate, fee structure, and consumer benefits.

| Rank | Card Name | Bank | Monthly Interest Rate | Annual Fee | Key Consumer Benefit |

| 1 | AUB Easy Mastercard | Asia United Bank | 2.00% | NAFFL | Lowest interest rate; choose due date + payment schedule |

| 2 | PNB Ze-Lo Mastercard | PNB | 2.50% | NAFFL | Zero late fee, zero overlimit fee; highly penalty-free |

| 3 | UnionBank U Visa Platinum | UnionBank | 3.00% | NAFFL | No late fees, no overlimit fees, 10% interest rebate |

| 4 | Citi Simplicity+ Card | UnionBank | 3.00% | NAFFL | Purely fee-free; no annual fee, no late fee, no overlimit fee |

| 5 | UnionBank Rewards Card | UnionBank | 3.00% | NAFFL | Strong rewards program (3 points per ₱30 spend) |

Detailed Analysis of the Top 5 Credit Cards

1. AUB Easy Mastercard

⭐ Best Overall: Lowest Interest Rate + Highly Flexible Payments

The AUB Easy Mastercard takes the top spot for one major reason: it offers the lowest monthly interest rate in the market at just 2.00%—a full point lower than the BSP cap.

Key Features

- 2.00% interest rate

- No Annual Fee for Life (NAFFL)

- Choose your billing cycle: weekly, semi-monthly, or monthly

- Choose your due date and payment amount

Why It Benefits Consumers

This card is perfect for anyone who wants maximum control over their budget. The ability to set your payment schedule makes it ideal for:

✔ Freelancers

✔ Commission-based workers

✔ Online sellers

✔ Budget-conscious consumers

The lower interest rate means you pay less when you can’t settle your full balance—giving you real breathing room during tight months.

2.PNB Ze-Lo Mastercard

⭐ Best for Fee Avoidance: Zero Penalties + Low Interest

True to its name, the PNB Ze-Lo Mastercard is designed to eliminate unnecessary costs. Its 2.50% interest rate is lower than the maximum allowed, and its “Zero Fee Policy” ensures you avoid costly penalties.

Key Features

- 2.50% interest rate

- No Annual Fee for Life

- Zero late payment fee

- Zero overlimit fee

Why It Benefits Consumers

This card is ideal for:

✔ First-time cardholders

✔ Those who worry about missing due dates

✔ Anyone who wants peace of mind

The absence of penalty fees helps cardholders avoid sudden, budget-breaking charges. Even if you slip up occasionally, your statement won’t explode with penalties.

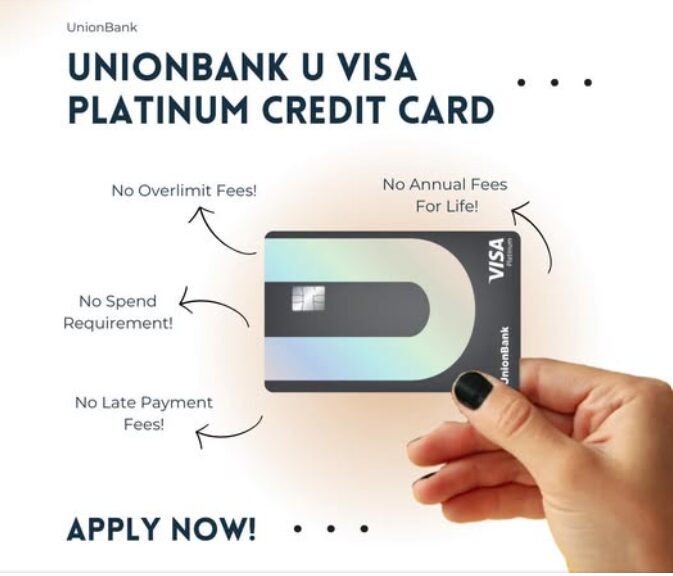

3. UnionBank U Visa Platinum

⭐ Best for Responsible Payers: 10% Interest Rebate

While the UnionBank U Visa Platinum charges the standard 3.00% interest rate, it stands out thanks to its 10% interest rebate for customers who pay on time.

This effectively lowers your cost without changing the official rate.

Key Features

- 3.00% interest rate

- NAFFL

- Zero late payment fees

- Zero overlimit fees

- 10% rebate on interest charges

Why It Benefits Consumers

This is perfect for consumers who:

✔ Usually pay on time

✔ Occasionally revolve their balance

✔ Appreciate rewards for responsible behavior

The interest rebate helps turn good payment habits into actual savings.

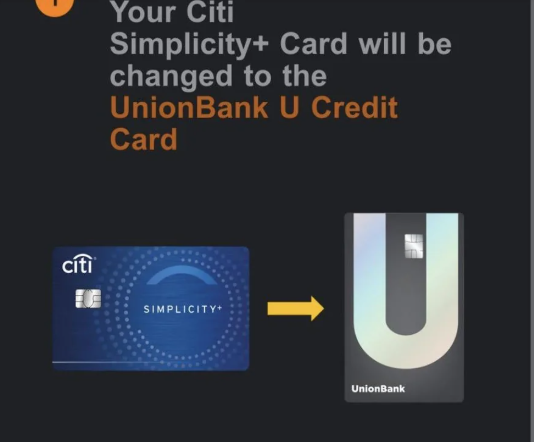

4. Citi Simplicity+ Card (Now Under UnionBank)

⭐ Best for Simplicity: Pure, Straightforward, and No Fees

The Citi Simplicity+ Card is famous for one thing: no nonsense, no surprises. It has:

- No annual fee

- No late payment fee

- No overlimit fee

And that level of simplicity is rare in the credit card world.

Key Features

- 3.00% interest rate

- NAFFL

- Zero penalty fees—forever

Why It Benefits Consumers

This card is perfect for Filipinos who:

✔ Want a stress-free credit experience

✔ Prefer a simple card with no complicated terms

✔ Don’t want to worry about penalties

While the interest rate is standard, the total removal of penalty fees gives cardholders predictable, transparent spending—making it a great choice for beginner and seasoned users alike.

. UnionBank Rewards Credit Card

⭐ Best for Everyday Spending: Rewards Without Fees

This card proves you can enjoy rewards and perks without paying an annual fee. With 3 points per ₱30 spend, the UnionBank Rewards Credit Card is great for daily purchases.

Key Features

- 3.00% interest rate

- No Annual Fee for Life

- 3 reward points per ₱30 spent on shopping and dining

Why It Benefits Consumers

This is ideal for:

✔ Frequent shoppers

✔ Diners and café regulars

✔ Consumers who maximize rewards

It lets you enjoy perks without the burden of renewal fees—a perfect mix of rewards + savings.

Overall Benefits of Choosing Low-Rate, No-Fee Cards

1. Lower Cost of Borrowing

Cards with interest rates below the 3.00% cap—such as AUB Easy (2.00%) and PNB Ze-Lo (2.50%)—directly reduce the cost of carrying a balance.

If you revolve ₱20,000 for a month:

- At 3.00% → ₱600 interest

- At 2.00% → ₱400 interest

That’s already a ₱200 savings per month, or ₱2,400 per year. For bigger balances, the savings grow even more.

2. No Annual Fees—Ever

Most Filipinos don’t realize that paying annual fees for 10 years means spending:

₱12,000 to ₱40,000+

…just to own a card.

NAFFL removes that cost entirely—making your credit card truly cost-efficient long-term.

2. No Annual Fees—Ever

Most Filipinos don’t realize that paying annual fees for 10 years means spending:

₱12,000 to ₱40,000+

…just to own a card.

NAFFL removes that cost entirely—making your credit card truly cost-efficient long-term.

3. Zero Penalties = Less Financial Stress

Cards like PNB Ze-Lo, UnionBank U Visa Platinum, and Citi Simplicity+ eliminate:

- Late payment fees

- Overlimit fees

This protects consumers from sudden financial hits during emergencies or unexpected expenses.

4. Rewards + Savings Combined

UnionBank Rewards shows that you can enjoy point earnings without paying annual fees—something rare among traditional Philippine credit cards.

Which Card Is Best for You?

There’s no single “best” card for everyone—only the card that best fits your lifestyle.

Choose AUB Easy Mastercard if you want:

✔ Lowest interest rate

✔ Flexible payment schedules

✔ Cash flow control

Choose PNB Ze-Lo Mastercard if you want:

✔ Low interest + zero penalties

✔ A beginner-friendly, stress-free card

Choose UnionBank U Visa Platinum if you want:

✔ Rewards for paying on time

✔ A premium but cost-free experience

Choose Citi Simplicity+ if you want:

✔ A straightforward, fee-free card

✔ Zero penalty fees—forever

Choose UnionBank Rewards Card if you want:

✔ Points and perks without annual fees

✔ A rewards card you can keep long-term

📚 Want the complete picture? Read our comprehensive guide: The Ultimate Guide to Credit Scores in the Philippines (2026) — covering everything from how CIC works to proven strategies for improving your score.

nn